Economic Blog

After carving out the first part of a “V-shaped” recovery, the US economy has leveled off somewhat in response to the latest wave of COVID-19 infections. In this week’s Weekly Market Commentary: Stalling Economic Recovery May Slow Stock Market Rally, we highlighted some evidence of a pause, mostly around mobility. We also cited the recent drop in seated diners from OpenTable and the leveling off of map requests for driving directions reported by Apple Maps, and several other data points.

“Most of the real-time data we follow reflects a pause in the recovery following the latest COVID-19 outbreak,” explained LPL Financial Equity Strategist Jeffrey Buchbinder. “We expect the stock market to follow the economic data and take a breather after a 45% rally in just four months.”

Several other high-frequency data points point to a pause in the recovery, including a few related to mobility and the pace of business reopenings.

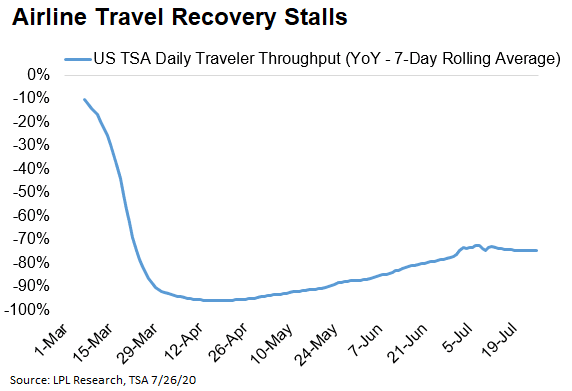

Air travel has edged lower in recent weeks amid renewed health restrictions and increasing concerns about COVID-19 outbreaks.

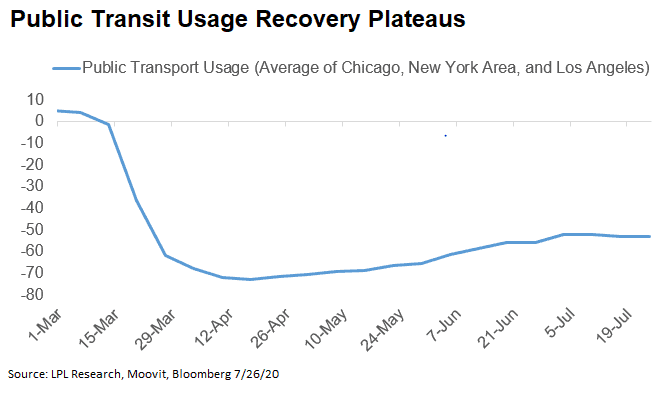

Use of public transportation has tailed off recently in some of the most populated cities in the country, reflecting business closures and increasing health concerns. Google’s announcement Monday that its employees would work from home until summer 2021 suggests this measure of economic activity may flatline for a while.

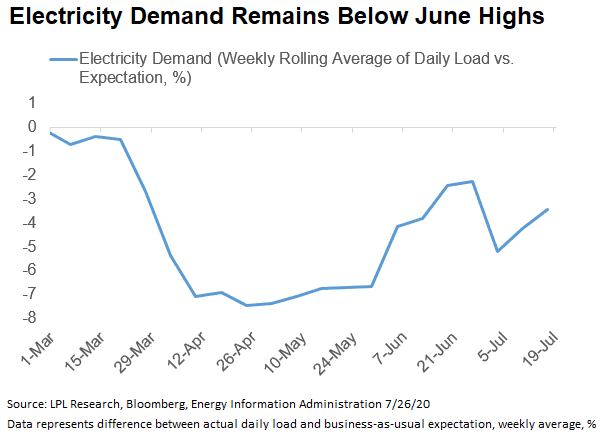

Electricity demand has fallen from its recent peak in mid-June, though the latest weekly data point rose slightly. Still, this is consistent with other data suggesting a slowdown in the rate at which businesses are reopening.

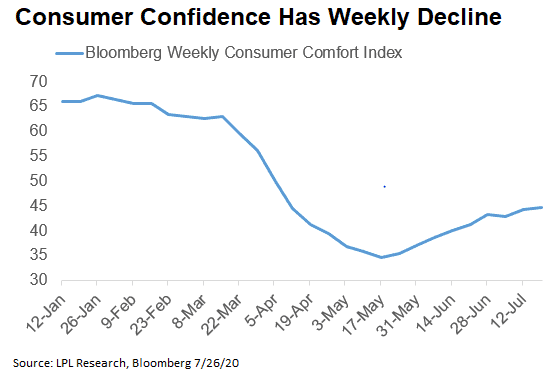

Some more traditional data points also tell the same story. First, the latest COVID-19 wave has flattened consumer confidence’s recovery trajectory based on Bloomberg’s weekly measure. Today we get the monthly consumer confidence reading from the Conference Board, which is expected to drop 3–4 points from the prior month.

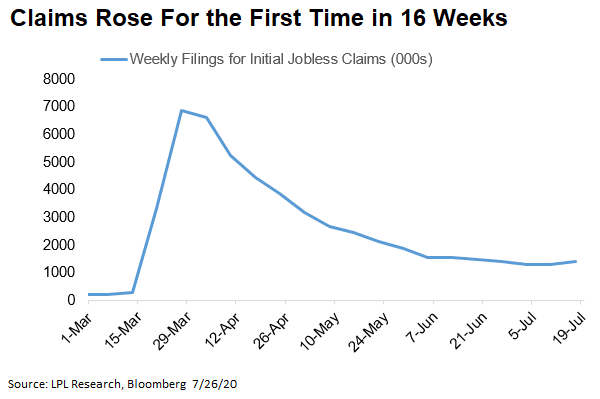

Weekly jobless claims rose for the first time in 16 weeks to over 1.4 million for the period ending July 18 and remain well above the pre-pandemic record high of around 700,000.

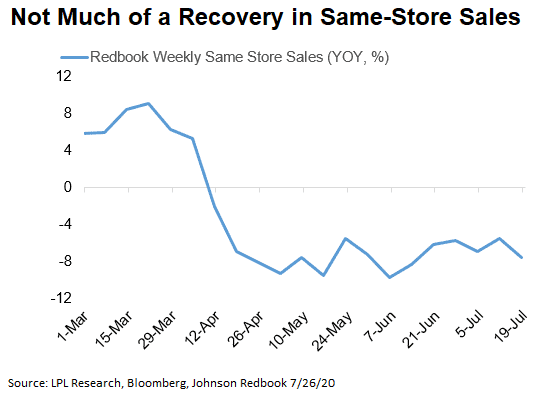

Same-store sales at retailers have hardly made up any ground over the past couple of months.

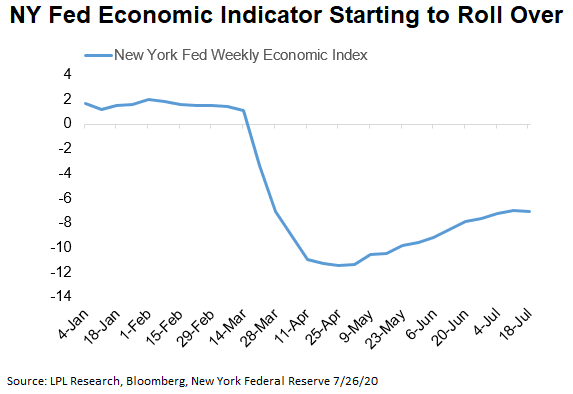

Finally, the New York Federal Reserve’s Weekly Economic Index has shown signs of rolling over in the latest reported week, which could indicate that the third quarter rebound in gross domestic product (GDP) that we expect may not be quite as sharp as many economists expect. The latest reading at -7, which implies an approximately 7% year-over-year decline in GDP, highlights how much ground the economy still has left to make up.

Given recent developments on COVID-19, including some renewed restrictions on public gatherings, it is not particularly surprising that some of these high-frequency data points have pointed to a pause. We knew the first leg of the recovery, like turning the lights on, was going to be the easy part. The key question now is how long it will take for these indicators to resume their climbs. More progress containing the virus in the latest hotspots in the South and West is probably necessary, though we are encouraged by falling daily infection rates in such places as Alabama, Arizona, Florida, and Texas.

LPL Research will continue to monitor these data points and other high-frequency data and provide timely updates.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All index and market data are from FactSet and MarketWatch.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use | Tracking # 1-05037957