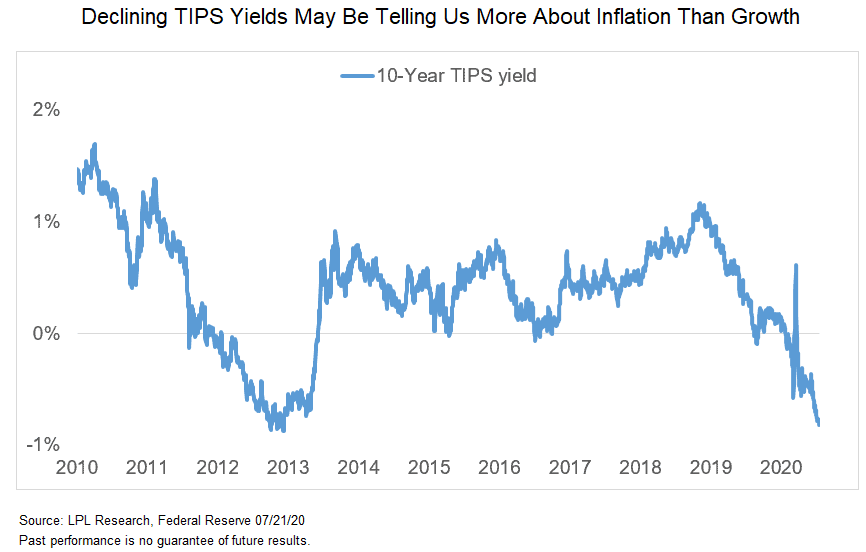

While the 10-year Treasury yield has traded in a narrow range since early April, the equivalent real yield, represented by the yield on 10-year Treasury inflation-protected securities (TIPS), has continued to fall and could go lower. Real yields remove the impact of inflation. As shown in the LPL Chart of the Day, while the 10-year Treasury set a new all-time low for yields way back in February, declining 10-year TIPS yields are still above where they were in late 2012.

Falling real yields tell a story. Often it means lower growth expectations, but it can also mean higher inflation expectations, especially with expectations coming off of low levels. It depends on whether investors are buying the safety of government securities or hedging against inflation. With central banks committed to keeping rates low, we think in this case changing inflation expectations may be an important part of the story.

“The bond market has not shown much confidence in the stock market rally,” said LPL Research Chief Market Strategist Ryan Detrick. “But with TIPS showing inflation expectations possibly creeping higher and credit spreads improving, it may be starting to listen.”

These conditions have been a good set-up for TIPS. Bond prices go up when yields fall, so still falling TIPS yields have been an important tailwind for TIPS returns while stagnant Treasury yields have capped Treasuries’ gains. The implied inflation expectations based on real yields fell to as low as 0.5% and is now a little under 1.5%, still low for the cycle but getting closer to normal, especially considering we’re still early in the recovery.

TIPS may still hold a small advantage over Treasuries but the big move has probably already happened. In the long run, the two tend to behave similarly. Over the last ten years, the Bloomberg Barclays US Treasury Index has returned about 3.4% annually, while the Bloomberg Barclays TIPS Index has returned 3.7%. The global economic recovery will take time, which will limit inflationary pressures, so there’s probably not a strong immediate need for inflation hedging, but we would still consider valuations compared to Treasuries attractive. TIPS, like Treasuries, are also sensitive to rising rates. But having some TIPS in the high quality bond mix can still make sense, especially for strategic investors.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results. All market and index data comes from FactSet and MarketWatch.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities. All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

This Research material was prepared by LPL Financial, LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC).

Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

- Not Insured by FDIC/NCUA or Any Other Government Agency

- Not Bank/Credit Union Guaranteed

- Not Bank/Credit Union Deposits or Obligations

- May Lose Value

For Public Use – Tracking 1-05035368